Big Data analytics in the banking sector

Vladimir Fedak Initially posted on company’s blog — https://itsvit.com/blog/big-data-analytics-banking-sector/

Big Data Analytics can become the main driver of innovation in the banking industry — and it is actually becoming one. We list several areas where Big Data can help the banks perform better.

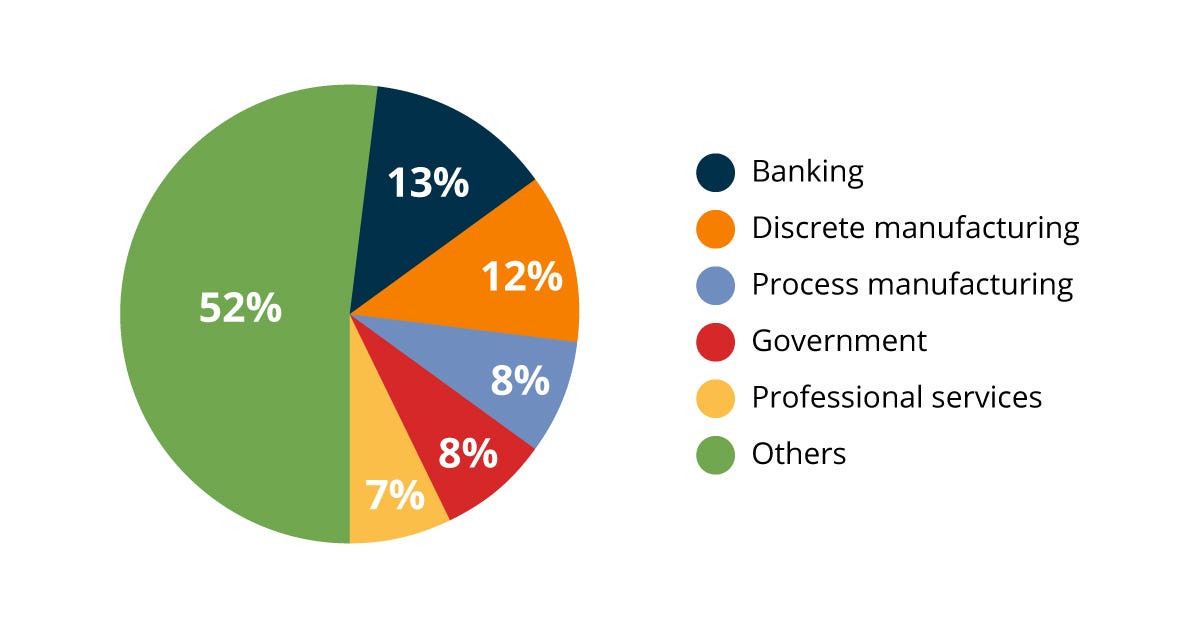

Investments in Big Data analytics in banking sector totalled $20.8 billion in 2016, according to the IDC Semiannual Big Data and Analytics Spending Guide of 2016. This makes the domain one of the dominant consumers of Big Data services and an ever-hungry market for Big Data architects, solutions and bespoke tools.

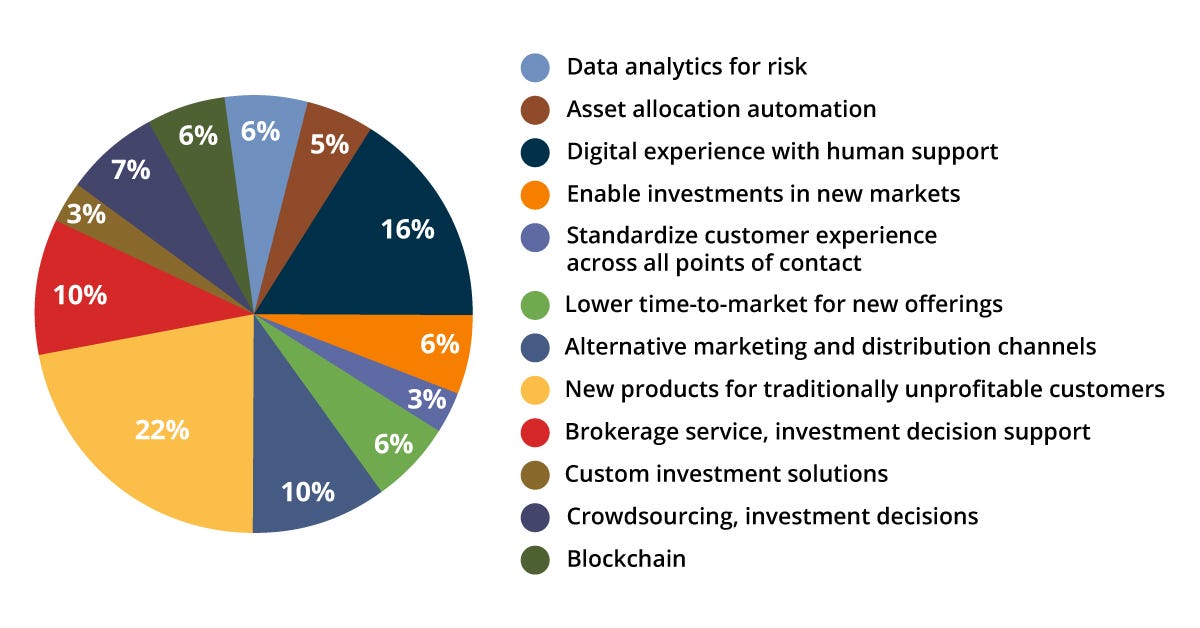

Within this wealth of investments, the allocation of funds mostly targeted the customer support, risk assessment, decision-making support and researching for new profit opportunities along with investing in new markets, lowering time-to-market and funding the blockchain projects, as the PwC Global FinTech Report, published March 2016, shows.

The trend is growing and in 2017 these numbers became only bigger. The amount of data generated each second will grow 700% by 2020, according to GDC prognosis. The financial and banking data will be one of the cornerstones of this Big Data flood, and being able to process it means being competitive among the banks and financial institutions.

As we already elaborated while listing the types of Big Data tools IT Svit uses, the really big data flows can be described with 3 v’s: variety, velocity, and volume. Here is how these relate to the banks:

- Variety stands for the plenitude of data types processed, and the banks do have to deal with huge numbers of various types of data. From transaction details and history to credit scores and risk assessment reports — the banks have troves of such data.

- Velocity means the speed at which new data is added to the database. Hitting the threshold of 100 transactions per minute is easy for a respectable bank.

- Volume means the amount of space this data will take to store. Huge financial institutions like the New York Stock Exchange (NYSE) generate terabytes of data daily.

However, as we explained in the article on the Big Data visualization principles, the 3 v’s are useless if they do not lead to the 4’th one — value. For the banks, this means they can apply the results of big data analysis real time and make business decisions accordingly. This can be applied to the following activities:

- Discovering the spending patterns of the customers

- Identifying the main channels of transactions (ATM withdrawal, credit/debit card payments)

- Splitting the customers into segments according to their profiles

- Product cross-selling based on the customers’ segmentation

- Fraud management & prevention

- Risk assessment, compliance & reporting

- Customer feedback analysis and application

Below we elaborate on the examples of using Big Data in these fields of the banking industry.

Customer spending patterns

The banks have direct access to a wealth of historical data regarding the customer spending patterns. They know how much money you were paid as a salary any given month, how much went to your saving account, how much went to your utility providers, etc. This provides a reach basis for further analysis. Applying filters like festive seasons and macroeconomic conditions the banking employees can understand if the customer’s salary is growing steadily and if the spending remains adequate. This is one of the cornerstone factors for risk assessment, loan screening, mortgage evaluation and cross-selling of multiple financial products like insurance.

Transaction channel identification

The banks benefit greatly by understanding if their customers withdraw in cash all the sum available on the payday, or if they prefer to keep their money on the credit/debit card. Obviously, the latter customers can be approached with the offers to invest in short-term loans with high payout rates, etc.

Customer segmentation and profiling

Once the initial analysis of customer spending patterns and preferred transaction channels is complete, the customer base can be segmented according to several appropriate profiles. Easy spenders, cautious investors, rapid loan repayers, deadline rush returners… Knowing the financial profiles of all customers helps the bank evaluate the expected spending and income next month and make detailed plans to secure the bottom line and maximize income.

Product cross-selling

Why not offer a better return on interest to cautious investors to stimulate them to spend more actively? Is it worth providing a short-time loan to an easy spender who already struggles to repay a debt? Precise analysis of the customers’ financial backgrounds ensures the bank is able to cross-sell auxiliary products more efficiently and better engage the customers with personalized offers.

Fraud management & prevention

Knowing the usual spending patterns of an individual helps raise a red flag if something outrageous happens. If a cautious investor who prefers to pay with his card attempts to withdraw all the money from his account via an ATM, this might mean the card was stolen and used by fraudsters. A call from a bank requesting a clearance for such operation helps easily understand if it is a legitimate claim or a fraudulent behavior the cardholder does not know of. Analyzing other types of transactions helps cut down the risk of fraudulent actions greatly.

Risk assessment, compliance & reporting

A similar procedure can be used for risk assessment while trading stocks or screening a candidate for a loan. Understanding the spending patterns and previous credit history of a customer can help rapidly assess the risks of issuing a loan. Big Data algorithms can also help deal with compliance, audit and reporting issues in order to streamline the operations and remove the managerial overhead.

Customer feedback analysis and application

The customer can leave feedback after dealing with the customer support center or through the feedback form, but they are much more likely to share their opinion through the social media. Big Data tools can sift through this public data and gather all the mentions of the bank’s brand to be able to respond rapidly and adequately. When the customers see the bank hears and values their opinion and makes the improvements they demand — their loyalty and brand advocacy grows greatly.

Final thoughts on using Big Data in the banking sector

Doing the things the old way is too risky nowadays. The companies must evolve and grasp the new technologies if they want to succeed. Adopting the Big Data analytics and imbuing it into the existing banking sector workflows is one of the key elements of surviving and prevailing in the rapidly evolving business environment of the digital millennium.

We are all used to perceive the banks as huge buildings with cool marble halls where the clerks work with the customers. In the last 10 years, the banks invested heavily into modernizing their offers and providing mobile access to their services. In the next 5 years, they will have to learn to empower their operations with Big Data analytics, AI/ML algorithms, and other high-tech tools.